PREVIOUS YEAR SOLVED PAPERS - July 2018

- Option : C

- Explanation : If an employee receives compensation (whether in one go or in installments) on voluntary retirement or separation, Section 10(10C) provides for exemption for such amount, subject to a maximum of Rs.5,00,000.

This exemption is available to employee of any of the following:

∎ A public sector company

∎ Any other company

∎ An authority established under a Central, State or Provincial Act

∎ A local authority

∎ A co-operative society

∎ A University established or incorporated by or under a Central, State or Provincial Act and an Institution declared to be a University under section 3 of the University Grants Commission Act, 1956 l An Indian Institute of Technology within the meaning of clause (g) of section 378 of the Institutes of Technology Act, 1961 (59 of 1961)

∎ Any State Government

∎ The Central Government

∎ An institution, having importance throughout India or in any State or States, a the Central Government may, by notification in the Official Gazette 82, specify in this behalf

∎ Such institute of management as the Central Government may, by notification 83 in the Official Gazette, specify in this behalf.

97. Which one of the following statements is not correct with reference to the assessment of firms?

- A

All partnership firms formed under the Indian Partnership Act, 1932, are assessed as firms under the Income Tax Act, 1961.

- B

Income of a firm is taxable at a flat rate of 30% without any exemption.

- C

Partners’ share in the income of a firm is not chargeable to tax in the hands of partners.

- D

Remuneration paid to partners of a firm (assessed as such) is allowed as deduction subject to statutory limit.

- Option : A

- Explanation : Tax on Income of a Partnership Firm and LLP:

∎ Income Tax at a flat rate of 30% is levied on Partnership Firms and LLP’s. Computation of taxes as per Income Tax Slab Rates is not allowed as the benefit of Slab Rates is only available to Individuals and HUF’s. Education Cess @2% and SHEC @1% would also be required to be paid. Moreover, in case the income of the partnership firm is more than Rs.1 crore in any financial year, Surcharge @10% would also be payable.

∎ Capital Gains arising from the sale of any asset by the partnership firm are taxable under Section 112. Moreover, in case of sale of shares and mutual funds, in case the period of holding is less than 1 year—the income would be taxable under Section 111A at a flat rate of 15% and in case the period of holding of shares is more than 1 year—the income would be exempted from the levy of tax under Section 10(38).

∎ Remuneration and Interest is allowed to be paid to the partners. However, the tax deduction for remuneration and interest paid to the partners is allowed subject to the limits and conditions specified in Section 40(b).

∎ Remuneration and Interest received by the partners shall be taxed in their hands as income under head PGBP. However, the salary and interest which have not been allowed under Section 40(b) or any other section shall not be added to the income of the partners.

∎ The share of the partners in the total income of the firm is exempt in the hands of the partners as the same has already been taxed in the hands of the partnership firm.

∎ Losses of the firm should be carried forward and not allowed to be allocated to the partners.

∎ Deductions under Chapter VI-A would be allowed from the Gross Total Income only for Donations or in case the business falls under the specified category of business.

∎ In case the partnership firm is unable to pay the tax dues, the partners can be held liable for recovery of the tax dues.

∎ It is pertinent to note that although LLP’s are treated in the same manner as Partnerships, there is only one section which does not apply to LLP’s and applies to Partnership Firms which is Section 44AD. LLP’s cannot claim benefits of Section 44AD by using Presumptive Taxation.

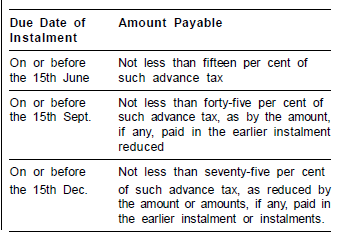

98. The due date of first instalment of advance tax by assessees other than companies is:

- Option : B

- Explanation : Section 211(1): Advance tax on the current income shall be payable by—all the companies, who are liable to pay the same, in four instalments during each financial year and the due date of each instalment and the amount of such instalment shall be as specified below: